With a growing number of governments encouraging their adoption, and more car manufacturers planning to produce a greater variety of models, electric vehicle (EV) investment has escalated in recent years.

January 25, 2019 In partnership with academia, Vulog for Education aims to forge long-term relationships in order to accelerate research on the mobility of the future, product/service innovations, and foster collaborations with cities.

Despite this, consumers have been slow to respond and EV sales have failed to gain traction in most countries, with battery EVs representing just under 1% of global passenger vehicle sales in 2017.

There are a number of factors that drive a mass adoption of electric vehicles, the most important of which are:

- Improved cost competitiveness with internal combustion engine (ICE) vehicles

- Access to public charging infrastructure

- Availability of EV brands and models

- Cost competitiveness with ICE vehicles

The most important driver of Electric Vehicle adoption is cost competitiveness with comparable ICE vehicles² on a total cost of ownership (TCO) basis. TCO is measured through a variety of factors, including purchase price (including taxes) and operating costs.

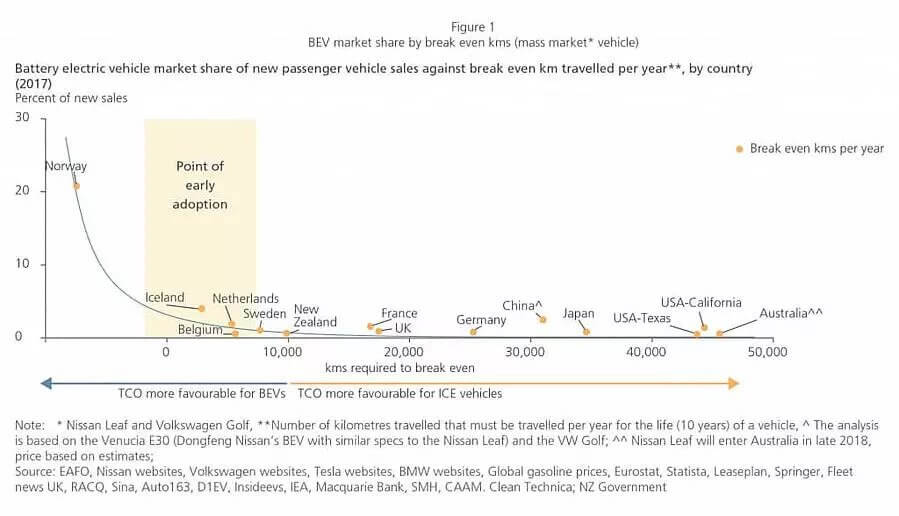

The purchase price for EVs is currently higher than for comparable ICE vehicles, but the savings that accrue in operating costs mean that the annual TCO reaches parity when a specific number of kilometers (km) are traveled. This distance is referred to as the km required to “break-even”, and the lower the break-even km, the more competitive EVs are on a TCO basis.

Analysis of 13 countries (Figure 1) demonstrates that the lower the break-even km, the higher the share EVs have of new vehicle sales. This shows that the point of early adoption occurs when the km required to break-even falls below c. 10,000 km a year.

A case in point is Norway, where the rapid rise in adoption of EVs followed the creation of favorable market conditions — most notably generous subsidies — resulting in EVs achieving better than cost parity with ICE vehicles and therefore negative break-even km.

Similarly, China has seen a significant increase in EV uptake over the past few years. China’s central and local governments have provided a range of incentives for EV uptake, including purchase tax exemptions and subsidies³ while the country’s zero-emissions vehicle mandate will require auto manufacturers to produce, import, or source credits for a growing percentage of EVs from 2019⁴.

This contrasts with most other countries, where EVs are not yet at cost parity and therefore are far from experiencing the adoption rates seen in Norway. A country such as Australia is well down the adoption curve, and it may take up to c.10 years until EVs reach market parity.

As cost economics improve, greater EV adoption is likely to occur as consumers become more aware of the total cost of ownership, through increased education and awareness about the actual cost of ownership.

Public charging infrastructure for EV Adoption

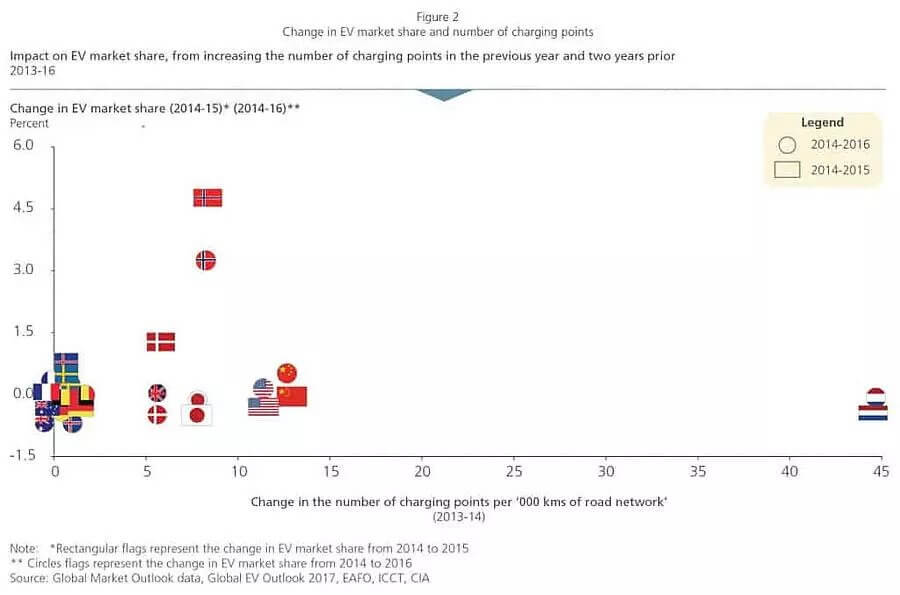

L.E.K. Consulting analysis suggests that, while public charging infrastructure is important, it appears to have had little effect in encouraging early adoption. Looking at the relationship between public charging infrastructure and subsequent growth in EV market share (one and two years later) across 12 countries (Figure 2), there is little correlation between investment in public charging points and increased EV adoption. This implies that the majority of current users have access to at-home charging and are likely to be dual car households or short-range travelers.

This suggests that large investments in public charging points will not in isolation drive EV uptake. However, in markets where there is limited access to home charging or where car owners are more likely to make long-distance or higher mileage trips (such as in the U.S. market), a lack of readily available public charging points will remain a barrier to uptake. To address this “range anxiety”, connecting cities with rapid public charging points along key highways should be prioritized, and in cities and towns, the focus should be on areas where cars are parked for the majority of the day (either at home or places of work) with slow charge options.

Availability of EV brands and models

The variety of available EV models will have an important impact on future demand. A growing number of car manufacturers plan to increase the number of EV models in the near future, providing customers with a greater choice — especially for mass-market vehicles. This will increase both competition and scale of production for EVs that, along with continued declines in the cost of batteries⁵, will put downward pressure on prices and increase their competitiveness.

An increase in the variety of EV models available means that customers will be more likely to find models that suit them, leading to word-of-mouth recommendations and fuelling further interest and adoption. The combination of falling prices with increasing suitability and convenience could mean that EVs are approaching the point where demand could materially increase.

Implications for original equipment manufacturers (OEMs) and policymakers

Cost competitiveness of EVs is the main factor in driving early adoption, but given the current size of the gap in price between an unsubsidized EV and an ICE vehicle, manufacturers need to focus on innovation and increased scale of battery production to bring down costs.

Furthermore, policymakers looking to drive early EV uptake should consider prioritizing incentives that lower the up-front purchase cost and increase consumer understanding of TCO.

As sales of EVs increase, governments are likely to scale back their level of support and manufacturers will need to be prepared to compete unaided with ICE vehicles. They will also need to demonstrate non-price value in less price-sensitive markets, such as luxury vehicles, by offering basic value-added services.

OEMs that ensure their EVs are competitive on a TCO basis, demonstrate high-end differentiation tailored to customers’ needs, and monetize home/public charging opportunities and battery storage solutions are likely to be successful in the EV market.

Author:

Monica Ryu, L.E.K. Partner

Contributing Authors:

Natasha Santha, L.E.K. Principal – Transport, New Mobility & Energy

Ashish Khanna, L.E.K. Partner

François Mallette, L.E.K. Managing Director and Partner

Vulog is the world’s leading tech mobility provider: we are committed to building a greener future, one city at a time.